FMP

Learn Financial Modeling (3/5): Discounted Cash Flow statement (DCF) Methodology

Sep 30, 2022

3. Find our Terminal Value

The terminal value (TV) of an asset, business, or project is the value of the asset, business, or project after the forecasted period when future cash flows can be estimated. Terminal value assumes that a company will continue to grow at a constant rate after the forecast period. The terminal value frequently accounts for a sizable portion of the total assessed value.

Forecasting value becomes more difficult as one looks further into the future. This is especially true when it comes to something as volatile as cash flow. However, it is critical to value businesses and assets as efficiently as possible, which is why financial models such as discounted cash flow are used to determine the total value of a project/business.

There are two methods used for terminal value calculations: The first is the perpetual growth method, which we will use. The perpetual growth method is based on the assumption that the growth rate of free cash flows in the final year of the initial forecast period will continue in perpetuity.

The second method is the multiple exit method. The multiple exit methods are predicated on assuming that a business will be sold after the projection period. To arrive at a terminal value, we will use the perpetual growth method.

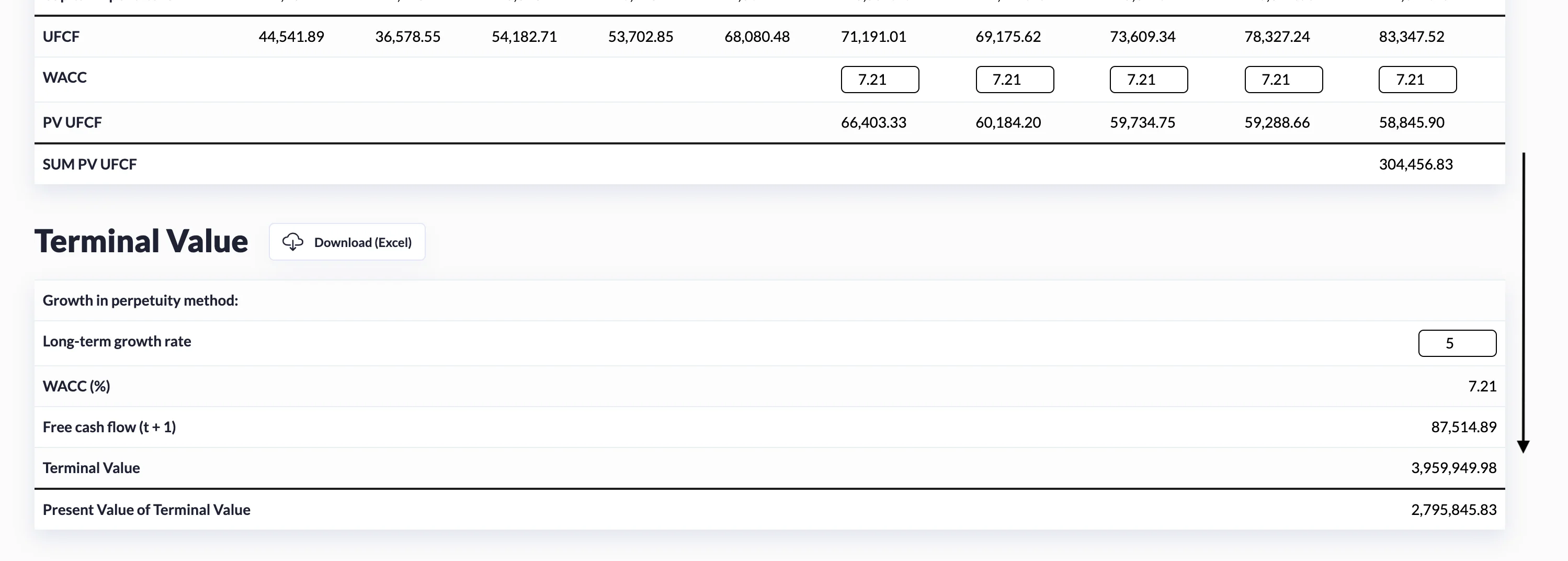

A terminal value is presumptively present in year 5. We will use the discount factor for year 5 to arrive at the present value of the terminal value. Let us proceed to calculate the terminal value now that we know what it is. We multiply the UFCF value from the forecasted year fivefold by one and add the long-term growth rate.

This calculation yields the value of the free cash flow (t+1). We will calculate the Weighted Average Cost of Capital (WACC) later, but to arrive at the terminal value, we would divide Free cash flow (t+1) by WACC minus the long-term growth rate.

Then, we divide the terminal value by 1 plus WACC raised to the fifth power to obtain the present value of terminal value.

In summary, we forecasted free cash flows from the present to the future to arrive at the present value of what we refer to as stage 1.

Then, using the perpetual growth method, we calculated the value beyond the explicit forecast periods. Then we discount that value to the present to obtain the terminal value's present value, which is the stage 2 value.

Next, we will learn how to calculate the WACC value; the only remaining factor we need to complete is the present values of the free cash flows and fill all the missing info in our DCF analysis. Go to weighted average cost of capital

Top 5 Defense Stocks to Watch during a Geopolitical Tension

In times of rising geopolitical tension or outright conflict, defense stocks often outperform the broader market as gove...

Circle-Coinbase Partnership in Focus as USDC Drives Revenue Surge

As Circle Internet (NYSE:CRCL) gains attention following its recent public listing, investors are increasingly scrutiniz...

LVMH Moët Hennessy Louis Vuitton (OTC:LVMUY) Financial Performance Analysis

LVMH Moët Hennessy Louis Vuitton (OTC:LVMUY) is a global leader in luxury goods, offering high-quality products across f...